The commercial real estate crisis is presenting significant challenges to the U.S. economy as high office vacancy rates continue to climb, impacting property values and investor confidence. As pandemic-induced shifts in work patterns persist, many urban office spaces are left unoccupied, leading to vacancy rates soaring between 12% and 23% in key cities. Financial experts warn that this downturn, exacerbated by rising interest rates, could trigger a series of bank failures as substantial real estate loans come due by 2025. With 20% of the colossal $4.7 trillion commercial mortgage debt maturing this year, the economic ramifications could be dire if delinquencies rise. As the financial landscape unfolds, it remains vital to monitor how these factors interplay, potentially setting the stage for a cascade of complications in the banking sector and beyond.

This ongoing situation in the commercial property market, often termed a real estate downturn, is underscoring the vulnerabilities facing financial institutions amid shifting economic conditions. With a substantial percentage of office spaces lying vacant and investor worries intensifying, the impact on regional financial entities could be profound. The combination of elevated office vacancy figures and impending debt maturities is causing analysts to rethink their views on loan stability, particularly regarding smaller banks. As interest rates remain unyieldingly high, the prospect of a major financial upheaval looms, compelling experts to assess the broader implications on the job market and consumer spending. Monitoring these early signs of distress could help safeguard against a more extensive economic fallout.

Rising Office Vacancy Rates and Their Impact on the Economy

The COVID-19 pandemic has drastically altered the landscape of commercial real estate, leading to a notable rise in office vacancy rates across major U.S. cities. With vacancy rates ranging from 12% to as high as 23% in places like Boston, the repercussions for the economy are profound. High vacancy rates typically depress property values, which, in turn, can impact local economies that rely on revenue generated from these real estate assets. Businesses that depend on foot traffic and commercial activity may struggle as fewer employees occupy office buildings, leading to a reduction in consumer spending in those areas.

As companies continue to embrace flexible work arrangements, the traditional demand for large office spaces is likely to remain diminished. Consequently, this prolonged high vacancy scenario has created a challenging environment for landlords and developers, who may find themselves facing increased financial strain. As property values decline, there is the potential for other economic sectors to feel the ripple effects, particularly in regions heavily invested in commercial real estate.

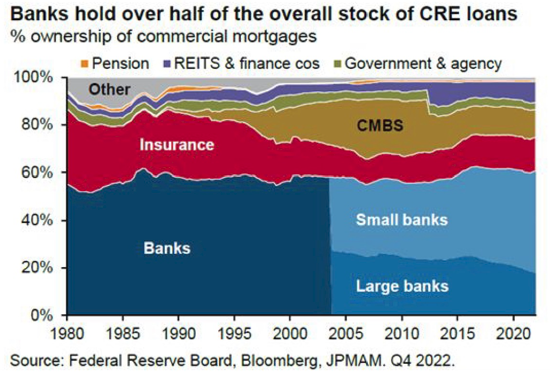

The Coming Wave of Commercial Real Estate Loans

The looming maturity of commercial real estate loans poses a significant risk to financial institutions, especially smaller banks that have been more heavily involved in this sector. With an estimated 20% of the $4.7 trillion in commercial mortgage debt coming due within the year, many analysts are closely monitoring how this wave of potential delinquencies could impact the banking landscape. Increased delinquency rates could lead to further bank failures and drive up the office vacancy rate as properties go into foreclosure, compounding the existing economic challenges.

Moreover, the stress in the commercial real estate loan market could create a ripple effect, where other sectors may be adversely affected. As banks grapple with losses on real estate loans, they may tighten lending criteria, making it more difficult for businesses and consumers to access credit. This could lead to reduced spending power and, ultimately, slower economic growth, particularly if regional banks—which account for a large share of commercial real estate lending—are destabilized.

The Economic Impact of Interest Rate Hikes

As the Federal Reserve maintains high interest rates, the implications for the commercial real estate market continue to unfold. Higher interest rates can significantly increase borrowing costs, making it more challenging for property owners to refinance existing loans. This situation not only affects current asset valuations but also places additional pressure on the overall economy. When property owners struggle to manage debt due to escalated financing costs, the risk of defaults rises, potentially culminating in a further increase in office vacancy rates.

Higher interest rates have traditionally been used to control inflation, but they can also have detrimental knock-on effects. Investors in commercial real estate, who once benefitted from low interest rates, now find themselves grappling with heavy debt loads as financing becomes costlier. This situation can lead to a market correction of sorts, thus impacting both consumer sentiment and the broader economic outlook, as businesses might delay expansion plans or reduce their workforce in response.

Banking Regulations and the Stability of Financial Institutions

In the aftermath of the 2008 financial crisis, banking regulations were significantly tightened, particularly for larger banks. These regulations have ensured that banking institutions maintain robust capital reserves to absorb potential losses, particularly in volatile sectors such as commercial real estate. As a result, while some smaller banks may be vulnerable to potential defaults on real estate loans, larger banks like JPMorgan Chase and Bank of America are better positioned to weather such storms, provided the issues remain contained.

However, the stress facing smaller banks exposed to the commercial real estate market could lead to forced industry consolidations, impacting competition and consumer choice. If these institutions begin to exhibit distress signals, larger banks may either acquire them or the Federal Reserve may intervene to prevent a systematic crisis, maintaining economic stability amidst challenging market conditions.

Potential Bank Failures and Their Broader Economic Repercussions

While the current projections indicate that a widespread banking crisis is unlikely, there is concern over the potential for localized bank failures due to their heavy reliance on commercial real estate lending. Excessive exposure to bad debts can diminish consumer confidence and prompt further economic contraction. The fear is that if several regional banks falter, it could trigger tighter lending standards across the board, further squeezing already beleaguered businesses and consumers.

The interconnectedness of the banking sector means that problems in one area can quickly escalate. If multiple banks experience crises related to commercial real estate loans, the resulting downturn could significantly impact spending and investment across various economic sectors. The cascading effects could create a more challenging environment for job growth and economic expansion, ultimately leading to a reassessment of strategies within both the banking industry and the broader economy.

Opportunities Amidst the Crisis in Commercial Real Estate

Despite the significant challenges presented by current high vacancy rates and the impending wave of matured loans, there are potential opportunities that could arise for savvy investors. Properties that are being sold at steep discounts could represent a chance to acquire prime assets at a lower cost, especially if the market stabilizes in the coming years. Investors capable of navigating the complexities of the commercial real estate landscape will find that there are still viable investment avenues, particularly those properties that can be retrofitted or repurposed.

Moreover, with a growing trend toward remote work, some office spaces may need to evolve into mixed-use properties that cater to changing consumer needs. This adaptability can create new revenue streams and opportunities for development. Investors and developers who can creatively pivot and respond to shifts in demand may emerge from this challenging landscape with profitable ventures, further stimulating economic recovery in the long run.

Learning from Past Financial Crises to Inform Future Strategies

The current commercial real estate crisis serves as a reminder of the lessons learned from past financial upheavals. During the 2008 financial crisis, the ripple effects of over-leveraged assets led to severe repercussions on banks and the economy as a whole. By leveraging historical data and trends, economists and financial professionals can better understand potential outcomes and devise strategies to mitigate risks inherent in the commercial real estate market today.

Financial institutions may benefit from reevaluating their lending practices and ensuring they maintain strict underwriting processes to avoid overexposure to risky loans. By learning from past mistakes, banks can safeguard against significant losses in times of distress. Additionally, broadening the base of assets beyond commercial real estate can help create a more stable financial environment, fostering overall economic resilience.

The Role of Pension Funds in the Commercial Real Estate Market

Pension funds are significant players in the commercial real estate market, often holding substantial real estate assets within their portfolios. As the market experiences fluctuations due to rising office vacancy rates and potential economic slowdowns, these funds face the dual responsibility of managing risk while ensuring returns for their members. The looming crisis in commercial real estate could place strain on pension funds as asset values decline, potentially leading to inadequate returns.

As pension funds adjust their investment strategies in response to shifting market conditions, they may opt to diversify away from traditional commercial real estate investments. This could involve allocating funds into other asset classes or sectors that demonstrate more stable returns. Ultimately, the performance of these funds in relation to commercial real estate will be closely monitored, as it directly impacts the financial well-being of future retirees and broader economic health.

The Future of Commercial Real Estate: Predictions and Considerations

As we look ahead, the future of commercial real estate remains uncertain, particularly with the significant challenges posed by high office vacancy rates and evolving workplace trends. The recovery of this sector will depend largely on macroeconomic factors, such as interest rates, employment levels, and lenders’ willingness to facilitate the necessary refinancing for maturing loans. Experts predict that adaptive reuse of existing properties may become a critical strategy for revitalizing certain segments of the market.

A shift toward more flexible and mixed-use developments could define new opportunities within the commercial real estate landscape in the coming years. Successfully navigating these changes will require innovative thinking and collaboration among stakeholders. As the commercial real estate sector adjusts to these new realities, its ability to pivot will ultimately determine its resilience and longevity in the economic landscape.

Frequently Asked Questions

How will the commercial real estate crisis affect office vacancy rates in the coming years?

The commercial real estate crisis is likely to exacerbate high office vacancy rates, especially in major cities. With current vacancy rates ranging from 12% to 23%, the ongoing downturn in demand for office space could lead to further declines in occupancy and property values, potentially dragging the economy down.

What potential impact does the upcoming wave of real estate loans maturing have on the commercial real estate crisis?

The looming maturities of nearly 20% of the $4.7 trillion in commercial mortgage debt could significantly intensify the commercial real estate crisis. As many borrowers struggle to refinance due to high interest rates, this may lead to increased defaults and financial strain on banks and investors.

Could the commercial real estate crisis trigger bank failures in the U.S.?

Yes, the commercial real estate crisis may result in some small and regional banks facing financial trouble due to significant exposure to delinquent real estate loans. While large banks are better capitalized and diversified, regional banks may struggle under the weight of rising defaults.

How are interest rates influencing the commercial real estate crisis?

Persistently high interest rates are a major contributor to the commercial real estate crisis as they make refinancing difficult for many properties. This scenario increases the risk of delinquencies on real estate loans, threatening the stability of the sector and the broader economy.

What are the economic implications of high office vacancy rates resulting from the commercial real estate crisis?

High office vacancy rates can lead to declining property values, which may harm local economies by reducing property tax revenues and limiting investment in urban areas. This decline, combined with potential bank losses related to real estate loans, creates a cycle that can negatively impact overall economic growth.

What strategies might mitigate the impact of the commercial real estate crisis?

Mitigation strategies for the commercial real estate crisis could include policies aimed at supporting refinancing options for struggling borrowers, aiding banks in managing their exposure, and possibly reimagining vacant office spaces to meet other housing needs in urban areas.

How is the economic impact of housing linked to the commercial real estate crisis?

The economic impact of housing is closely tied to the commercial real estate crisis, as high vacancy rates in commercial spaces can lead to reduced demand for housing. Additionally, defaults on real estate loans can create ripple effects, influencing housing market stability and consumer confidence.

What role do regional banks play in the commercial real estate crisis?

Regional banks are particularly vulnerable in the commercial real estate crisis due to their significant investments in real estate loans. As default rates increase, these banks may face considerable financial distress, affecting their ability to lend and potentially leading to broader impacts on local economies.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates range from 12% to 23% in major U.S. cities, impacting property values. |

| Surge of Debt Maturing by 2025 | 20% of $4.7 trillion in commercial mortgage debt comes due this year, raising concerns of bank losses. |

| Impact on Banks | Larger banks are well-capitalized post-2008; smaller banks could face difficulties without federal assistance. |

| Potential for Widespread Failure | Not likely to create a full-blown financial crisis, but significant losses are expected, especially for smaller banks. |

| Global Economic Outlook | The global economy remains solid, providing a buffer against potential real estate market downturns. |

| Factors Behind the Crisis | Over-leveraging and unexpected rise in interest rates exacerbated by pandemic-related demand drops. |

| Consequences for Consumers | Potential pain for consumers primarily through pension funds and regional bank lending conditions. |

| Investors’ Optimism | Belief that interest rates will eventually decrease, allowing refinancing options. |

Summary

The commercial real estate crisis poses significant challenges for the economy in 2024. High office vacancy rates and a surge of debt maturing by 2025 raise concerns over potential bank failures and broader economic repercussions. While experts suggest the situation won’t lead to a financial meltdown akin to the 2008 crisis, the repercussions on smaller banks and their consumers could be profound. As businesses navigate this evolving landscape, the potential for widespread impacts on both consumers and regional banks underscores the importance of monitoring the commercial real estate crisis closely.

Comments are closed, but trackbacks and pingbacks are open.